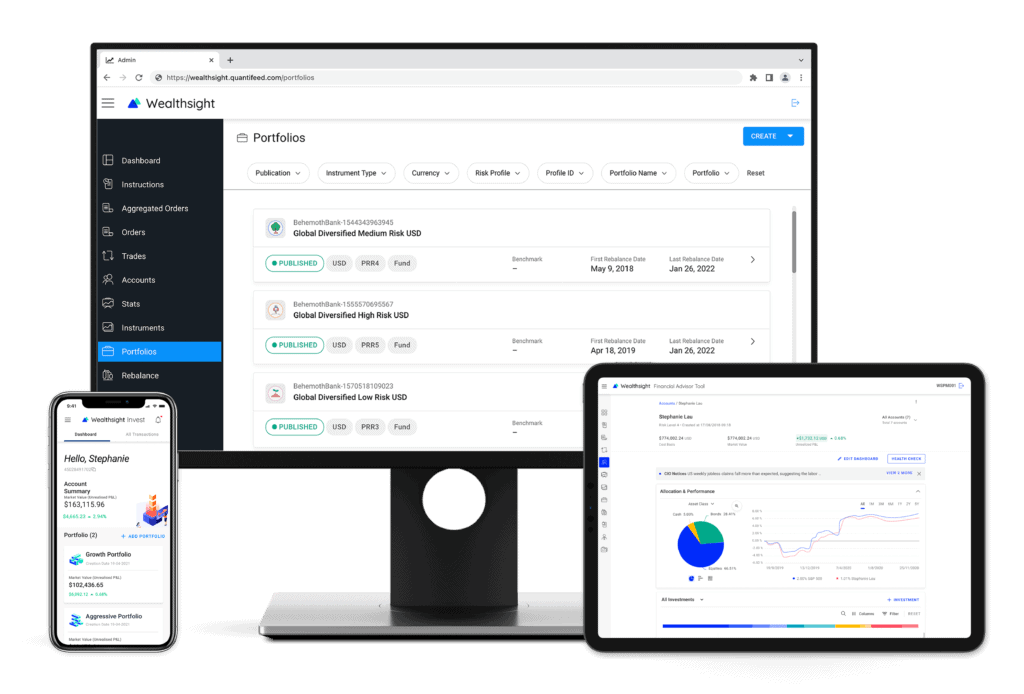

Powering next generation digital wealth platforms for financial institutions

Combining software engineering and quantitative finance, Quantifeed helps transform financial institutions into providers of wealthcare, a customer-centric service focused on meeting everyone's wealth management needs.

Quantifeed’s solutions bring benefits to customers, advisors, and portfolio managers. Our suite of functions is assembled and configured to create compelling digital advice propositions.

Quantifeed’s solutions empower CIOs, customers, advisors, and portfolio managers. Our suite of capabilities and services can be assembled and configured to create compelling digital advice propositions.

Our award-winning technology powers wealth management platforms to deliver engaging investment experiences at scale.

Build compelling wealth management propositions to service more customers, introduce efficiencies and grow your business.

WHY QUANTIFEED

The leading digital wealth management experts

We don’t just provide a platform, we deliver a total package. An end-to-end solution that includes all the necessary services that encompass intuitive design, sophisticated quant solutions, comprehensive portfolio analytics and continued consultation services. Our proven track record and strong understanding of the region’s business practices make us the best in the business.

Trusted by major financial institutions in the region, we understand the subtleties, regulations, and investment frameworks that enable our partners to transform and scale their wealth management business.

End-to-end Technology

As wealthcare experts, we simplify the complex back end and technology orchestration, presenting it as an easy and effortless way for customers to enjoy their investment journey.

Proven Track Record and Delivery

We know what it takes to launch a frictionless digital investment service. We deploy in any environment and can be set up and be ready to go quickly.

TECHNOLOGY

Configurable and modular technology for successful solutions

QEngine follows a modern architecture of loosely coupled services that are organised into multiple service layers. The platform uses an API-first and future-proof technology to enable multiple deployment models and deliver value to your business.

We use Cookies to enhance your online experience. By agreeing, you accept our Cookie Policy, Click 'Accept All Cookies' or 'Manage Cookies Settings' to choose specific preferences. You can update these settings anytime.

When you visit any web site, it may store or retrieve information on your browser, mostly in the form of cookies. Control your personal Cookie Services here.

Ross Milward leads Quantifeed’s technology and engineering efforts to deliver innovative digital wealth management solutions. Before co-founding Quantifeed, he spent more than 15 years in investment banking, holding senior positions in equity and equity derivatives technology.

His expertise is in developing and managing large-scale enterprise-level global trading and risk systems. A former managing director, Ross has worked for Bank of America Merrill Lynch and Deutsche Bank. He has held multiple global and regional leadership roles, most recently as head of equities technology in Asia. He has worked in Hong Kong, Sydney and London.

Ross holds a Bachelor’s degree in Computer Science with Honours and is a Fellow of the Securities Institute of Australia. He likes pushing his limits through long distance triathlon races.

Gary Wheeler

Chief Commercial Officer

Gary leads Quantifeed’s global commercial strategy, working closely with teams across Asia and the UK to strengthen go‑to‑market execution and deepen partnerships with financial institutions across Asia and EMEA.

He brings over 25 years of experience in financial services and investments, having held senior leadership roles at FE fundinfo, EV, and Lipper. Throughout his career, Gary has built a strong track record in delivering flagship commercial deals, driving revenue growth, and scaling international businesses.

Matt Johnson

Commercial and Business Development Lead

Matt Johnson is responsible for leading the commercial and business development efforts for EMEA, where he drives sales and partnership initiatives. With over 30 years of experience in Global Markets, Asset Management, and Financial Technology Sales, Matt brings a wealth of expertise to his role.

Throughout his career, Matt has demonstrated his ability to effectively manage European and global equity derivatives and exchange traded product sales teams, as well as holding executive committee and broader management positions. His entrepreneurial spirit and investment acumen have further motivated him to invest in multiple start-ups and Fintech companies.

Junyi Liang

Head of Japan Delivery

Junyi Liang leads Quantifeed’s Japan Delivery function, partnering closely with clients and colleagues to drive successful outcomes and support the company’s continued growth in the region.

He brings over 30 years of technology experience across financial services and insurance, with expertise spanning digital platforms, enterprise architecture, infrastructure, databases, and large‑scale technology delivery.

Thomas Barnes

Head of Application Engineering

Tom Barnes oversees the Application Engineering team at Quantifeed EMEA. He is responsible for technology and platform architecture across the organisation, optimising the scale and performance at which the platform operates.

Tom has twenty years of tech experience. In his career to date he has architected, delivered and scaled systems across a range of industries, built on a variety of technology stacks. Immediately prior to joining Quantifeed, Tom was a part of an award-winning startup, designing and delivering location-based services used by police and armed forces across Europe.

When he’s not studying for his MBA, he can usually be found walking, running or cycling around the forest in Epping, where he lives with his partner and their three children.

Alastair Smith

Head of Quantitative Solutions

Alastair Smith spearheads Quantifeed EMEA’s Quantitative Solutions team. Alastair and his team’s extensive knowledge of quant finance and trading strategies allows Quantifeed to develop cutting edge investment products to effectively serve its growing portfolio of global clients and partners.

Prior to joining Quantifeed, Alastair worked as an academic at Cambridge University, where he researched moment problems and stochastic solutions to integro-partial differential equations in very large numbers of dimensions. He holds a doctorate in stochastic modelling and a degree in mathematics both from the University of Cambridge.

Outside of work, Alastair has keen interests in travel, rowing, cycling, chess and cryptoassets.

Claire Percy

Head of Finance, EMEA

Claire Percy heads up the EMEA finance function overseeing financial processes and reporting. She works closely with the wider team to ensure day-to-day business efficiencies.

Working across a variety of different industries including management consultancy, outsourcing, manufacturing, digital media, Claire has gained valuable commercial and operational experience to deliver high quality reporting and analysis to aid better information and decision making.

In her free time, Claire balances the chaos of family life with her love of outdoor adventuring; running, hiking and wild-water swimming.

Dorothée Servant

Head of Product Management

Dorothée Servant leads as Head of Product Management at Quantifeed EMEA. She works closely with the product and engineering teams as well as on the client side to ensure the smooth delivery of high-quality client solutions. Her team is responsible for managing the complete life cycle from the initial specification phase to the final delivery, including the planning, execution, and testing phases.

Before joining Quantifeed, Dorothée worked as project owner at THALES, a French multinational company, interacting with all the Business Units in Europe. She holds an MBA from IESE Business School, and a master’s degree in civil engineering from l’Ecole Nationale Supérieure des Mines de Nancy.

Ananth Prabhu

Senior Program Manager

Ananth is the Senior Program Manager at Quantifeed. He has a wealth of experience in finance and operations with a track-record of building and managing successful client facing teams in global organisations. His team is responsible for onboarding and closely supporting Quantifeed’s portfolio of clients. He leads various aspects of client relationships as well as client training, product adoption and retention.

Prior to Quantifeed, Ananth worked at Morgan Stanley and was principally responsible for building and scaling the sales-trading desk for structured products across Morgan Stanley’s clients base in EMEA.

His time outside of work is mainly spent with his wife and two young children. He is passionate about travel, cuisine, sport, in particular football and scuba diving.

Karen Tierney

Head of Product Proposition

Karen Tierney leads Quantifeed EMEA’s Product Proposition team. She works closely with all teams across the organisation to evolve the product offering. She is responsible for ensuring the platform-wide strategy is aligned to customer’s needs, and our product build is prioritised, planned and executed effectively.

Trained as an Operations Research and Statistics Engineer with a Masters in Management, Karen brings a wealth of experience in product and programme management having delivered multifaceted client, regulatory and technology change projects. She joined Quantifeed from DWS and previously worked at RBS, Barclays, Deloitte and The National Bank of New Zealand.

Geoff Langham

Head of EMEA

Geoff Langham manages the Quantifeed EMEA team based in London and co-founder of Alpima. He is responsible for implementing the company’s infrastructure and its strategic direction. He has worked closely with all teams to successfully deliver solutions to its global clients and partners.

A twenty seven year veteran in the Finance industry, Geoff brings a wealth of experience from a trading and management perspective. Raised and educated in Canada at Queen’s University, he relocated to London to complete his MSc in Financial Economics. He began his career at JP Morgan trading FX/Rates following onto Morgan Stanley on the buy and sell sides as an equity trader. For the past 15 years, Geoff has held Board positions and COO roles at several fast growing financial companies.

In his spare time Geoff is a keen tennis player, powder skier, aspring chef and father to his three daughters.

Deepshikha Chaudhary drives sales initiatives for Quantifeed Singapore. She is responsible for building and growing the company’s presence in Southeast Asia. Prior to Quantifeed, Deepshikha worked with various financial technology providers leading business expansion in the region. She also has hands-on experience in the product development of a cloud-based trading and execution platform for Asia and Europe. Deepshikha has over a decade of experience in the finance industry.

Deepshikha holds a Bachelor of Technology in Computer Science and a Masters of Business Administration in Finance from Singapore Management University. To get her going, she likes to run, practice yoga and go surfing.

Vincent Emond

Client Success Lead

Vincent Emond leads Quantifeed’s client success team, designing compelling business proposition and driving client experience to ensure they achieve their desired outcomes.

Vincent has 15 years of experience spearheading innovative digital products in banking, insurance, and tech industries. Before joining Quantifeed, Vincent led product development and management for several HSBC digital platforms, including their flagship retail banking app in Hong Kong. He was also AXA’s Head of Digital Centre of Excellence, where he helped launch AXA’s first blockchain-powered insurance product. As a technically proficient digital consultant gifted in interpersonal relationships, one of Vincent’s most valuable skills is in bridging customer needs with complex technological solutions.

Vincent holds a Bachelor’s degree in Business and Marketing and a Master of Business in E-Commerce. Outside of work, he can be found climbing steep hills on his road bike as he strives towards his goal of breaking local Strava cycling records one segment at a time.

Rachel Liu

Head of Marketing & Communications

Rachel Liu leads Quantifeed’s marketing and communications initiatives. She is responsible for creating and accelerating the company’s marketing strategy and brand recognition across the region. Her expertise is in brand management and building global product campaigns. Prior to joining Quantifeed, Rachel built and executed marketing strategies at notable technology companies servicing business and retail sectors across Europe, US and Asia Pacific.

Rachel holds a MSc in Media and Communications from London School of Economics and Political Sciences and a Bachelor of Fine Arts from New York University.

Sharon Tang

Sales Director, NA

Sharon Tang leads sales and business development activities in the North Asia region at Quantifeed. Based in Hong Kong, she works closely with financial institutions across the region to help them develop their digital asset management capabilities. She has over a decade of experience in the finance industry and previously held senior regional sales positions at Osttra (formerly part of IHS Markit) and FIS.

Sharon holds a Bachelor’s degree in Business Administration from the University of Science & Technology in Hong Kong and a Master’s degree in Corporate Communications from IE Business School in Spain.

Michael McDonald

Head of Web Engineering

Michael McDonald builds Quantifeed’s online wealth management web application in order to deliver a user-friendly and integrated experience. Michael has over 11 years of experience in web application development.

As Developer for Crossroads Hong Kong, he and his team set up the infrastructure for its donation and stock management application. As Developer at e-commerce company Synapse Connect in New Zealand, he and his team helped clients build mobile applications like prospersoftware.nz, providing him with a full-stack web development and DevOps skillset, servicing clients and back-office operations.

Michael holds a Bachelor degree in Electrical and Computing Engineering from University of Canterbury New Zealand. He moved to Hong Kong in 2014 and enjoys the outdoors sports such as hiking and cycling.

Joy Sun

Head of Quantitative Engineering

Joy steers Quantifeed’s research and development in systematic investment strategies, portfolio construction and trade execution. Prior to joining Quantifeed, she worked as a quantitative analyst in asset management and proprietary trading firms.

She led development of trading strategies, including design,simulation and risk control, and research in market trend recognition and prediction. Joy earned her PhD in Operations Research from the University of Hong Kong, her MS in Statistics from Nan Kai University and her BS in Computational Mathematics from Dalian University of Technology.

John Threlfall

Head of Site Reliability Engineering

John leads the SRE team in Singapore and is responsible for the overall infrastructure and SDLC of Quantifeed’s technology platform, QEngine. He ensures the design, availability, and reliability meets the requirements of both our internal and external users. He has over 20 years’ experience in the banking industry, with a demonstrated history in transforming back-office technology and developing reliable engineering systems for large financial institutions.

Prior to joining Quantifeed, John held technical and leadership roles at Bank of America Merrill Lynch and Standard Chartered Bank. He holds a BSc degree in Artificial Intelligence from The University of Manchester in the United Kingdom. John moved to Singapore in 2008 and enjoys travelling with his family, football and scuba diving.

Lars Bischoff

Head of Core Engineering & Australia Country Lead

Lars Bischoff is a lead senior software engineer on Quantifeed’s back-end services, with a focus on trading and external interfaces.

Before joining Quantifeed, Lars had a number of leadership roles across major investment banks including Deutsche Bank, JP Morgan, UBS, and Citi. These roles included designing and implementing systems for Equities and Equity Derivatives Trading. Lars also held roles as country lead for Equities and Equity Derivatives Technology, as well as global lead for Equity Derivatives Trading.

As a former Executive Director in Deutsche Bank and JP Morgan, Lars has extensive experience in building local and global development teams. In this capacity, he also defined and realised the technology direction and innovative platforms in the Equity and Equity Derivatives space for these two organisations. Lars holds a Bachelor of Science degree in Computer Science, from Macquarie University, Sydney.

Chetan Shetty

Head of Product

Chetan leads Quantifeed’s product management capability and drives the implementation of features in our product that continuously solve digital wealth management problems for our clients.

Chetan started his career as a software engineer in the aerospace industry working across the entire software development lifecycle. Subsequently he worked in various roles helping large enterprises in Hong Kong solve business problems with process and technology solutions. His experience ranges across aviation, insurance, public sector services and consulting. He has lived and worked across multiple countries and enjoys travelling to new places, tasting new cuisines and occasionally writing his blogs.

Parul Srivastava

Head of Delivery & Singapore Country Lead

Parul Srivastava leads Quantifeed’s Delivery function. She enables Quantifeed customers to successfully adopt and launch innovative digital wealth management solutions. Parul brings 18 years of strong experience in the financial services industry, her knowledge edges across the delivery lifecycle and wealth domain areas including AML, KYC, client onboarding and Payments. She is experienced in managing complex , high value enterprise level programs with leading Banks like SCB , BNPP, OCBC and Technology Service providers like Cognizant, BAE Systems , Fenergo. She has worked vastly for APAC and EMEA region deliveries primarily based out of Singapore.

Parul Holds a Master’s in Business Administration in Finance and Accounting and is Certified PMI- Project Management Professional, Scaled Agilist, Scrum Master(CSM) and Product owner (CSPO). Beyond work she is interested in Art and Travel.

Conor Doyle

Head of Pre-Sales

Conor has over 20 years’ experience working in the Japanese market leading sales and service teams in high-growth financial software vendor organisations. He is bilingual (fluent in Japanese and English), with strong technical and integration experience and a proven track record of meeting targets, overcoming challenges in real time, and delivering tangible results.

Conor is an expert presenter, negotiator, and business operations manager. He is able to forge strong relationships with both clients and partners and build consensus across multiple organisational levels. Conor has demonstrated capacity for leadership and project management. His previous work experience focuses on leading multinational, cross-functional teams in the provision of leading-edge, highly complex and high-value fintech business solutions. Conor has a Mechanical Engineering degree from University College Dublin.

Robert Rice

Chief Sales Officer

Robert Rice leads Quantifeed’s sales strategy and works with clients to define and deliver digital wealth management solutions. Based in Hong Kong for over 15 years, Robert has held sales leadership roles in APAC and EMEA at London Stock Exchange Group (formerly Refinitiv), Fitch Solutions, OFX and SNL Financial, leading teams servicing wealth managers, asset managers and financial institutions.

His career is focused on brining innovative platforms, products and solutions to market helping clients meet their objectives. Robert is an appointed Mentor for the Hong Kong Fintech Week advising start-ups and market entrants on various topics and go to market initiatives.

Audrey Wong

Chief Operating Officer & Chief Financial Officer

Audrey Wong manages operations and financial affairs to deliver on Quantifeed’s business strategy. Audrey joined Quantifeed from Bank of America Merrill Lynch, where she was COO for the equities division in Asia Pacific. Audrey’s tenure at Merrill Lynch included senior assignments in Toronto and New York, before relocating to Hong Kong in 2006 to take a new role as the Finance Head of Equities Derivatives for APR.

Her responsibilities expanded to CFO of APAC Equities in 2011 and CFO for APAC Global Markets in 2013. Audrey holds a Bachelor of Business Administration from Brock University of Ontario. She is also a Chartered Professional Accountant of Ontario and Chartered Financial Analyst. Audrey enjoys biking and swimming with her two children.

John Robson

Principal Advisor

John Robson serves as Quantifeed’s Principal Advisor. He works with financial institutions to assist them in developing their digital wealth management future. Based in Hong Kong for over 30 years, he has held regional leadership roles at JP Morgan, Nomura and Merrill Lynch managing teams which serviced the region’s consumer and private banks.

His career has been focused on the development of investment platforms and products. He has been instrumental in introducing significant product innovation to wealth management platforms in Hong Kong, London and Tokyo.

Alex Ypsilanti

Chief Executive Officer & Co-Founder

Alex Ypsilanti spearheads Quantifeed’s mission to solve the challenges of digital wealth management.

Before co-founding Quantifeed, he spent fifteen years as an investment banking research analyst. His work enabled investors to improve their risk-adjusted returns and to gain access to a wider range of market strategies and risk premia. Alex, a top ranked analyst by Institutional Investor, had a leading role in the growth of the European ETF market, hedge fund replication and the use of volatility products in portfolios.

A former managing director for Morgan Stanley and Bank of America Merrill Lynch, Alex has built and led teams of derivatives and quantitative strategists in London, Tokyo and Hong Kong.

Alex holds Bachelors and Masters degrees in Information Systems Engineering and a PhD in Mathematical Finance from Imperial College, University of London.